SPWH: A Post-COVID Deer in Headlights

Going forward, we plan on occasional posts like this where we don't do a deep-dive, but provide high level thoughts on idiosyncratic situations we are watching.

Summary

- SPWH is facing a post-COVID hangover with weak sales trends and declining margins after opening too many stores.

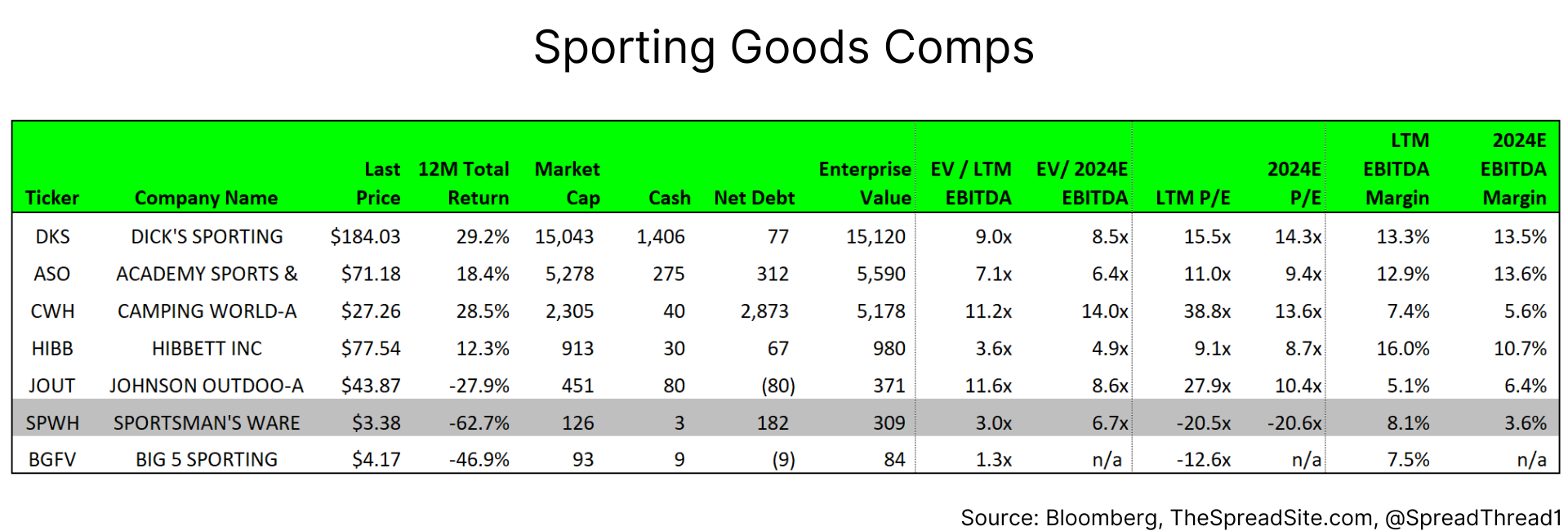

- We don't currently view the equity as cheap on an EBITDA basis (6.7x forward estimates) or at a 53% discount to book value as this metric is usually irrelevant for a retailer.

- SPWH could be an interesting distressed play at lower prices given a strategic buyer that may come back to the table or a scenario where an investor provides capital to fund an out-of-court restructuring.

Introduction

In today’s post we look at a former COVID beneficiary, Sportsman’s Warehouse “SPWH.” They are a micro-cap retailer primarily selling sporting goods (including guns) to outdoor enthusiasts. The closest peers would be Bass Pro Shops or Cabela’s, which are both are privately owned by Great Outdoors, LLC. After a surge in business during COVID the company has struggled and shares are currently trading around all-time lows.

SPWH has the potential to be an interesting distressed play on the equity should the company hit a liquidity crunch. We are not making that prediction, but liquidity could get tight assuming financial results in 2024 are like 2023. Further, SPWH states in their annual report that:

…the majority of our customers are male, between the ages of 35 and 65, and have an annual household income between $40,000 and $100,000.”

As we have discussed in our macro reports, this lower income cohort is currently under pressure.

Background on Sportsman’s Warehouse

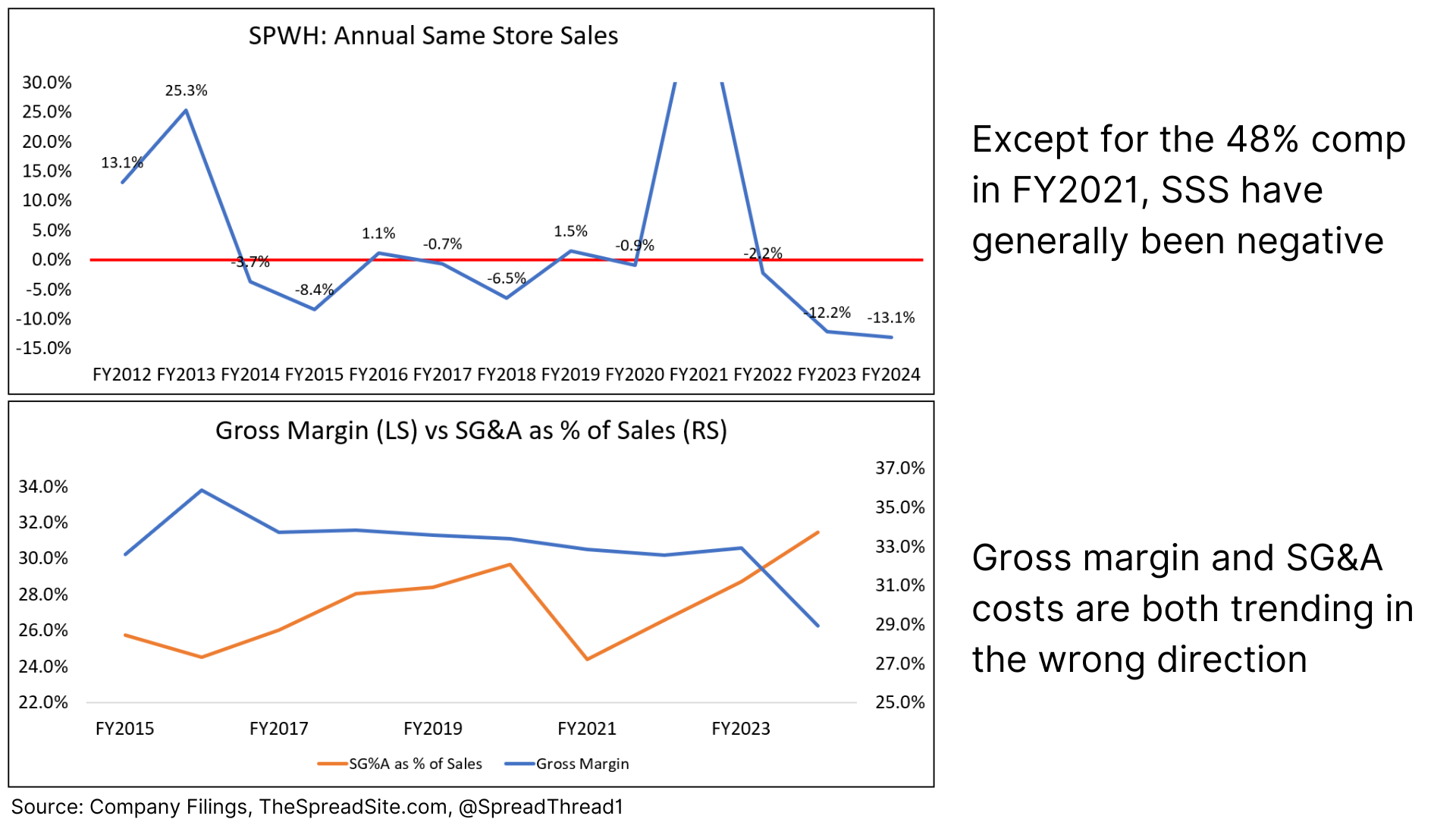

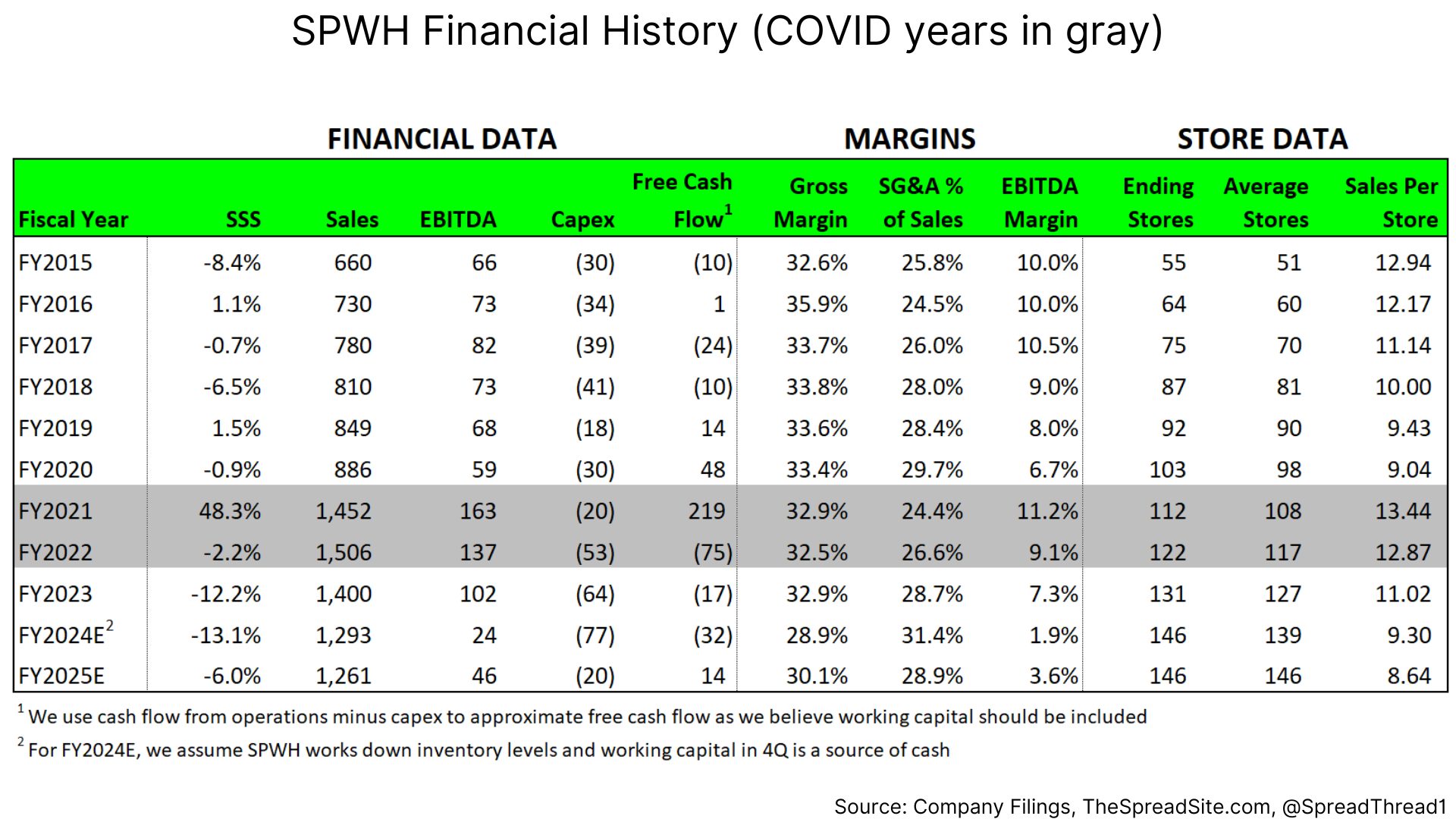

SPWH has faced a somewhat tumultuous history. In 2009, as a private company, they filed ch.11 and were subsequentially acquired out of bankruptcy by Seidler Partners. Then in 2014 they were taken public and performance was generally lackluster until COVID hit and comps surged to 48%. There was a failed buyout attempt in 2020 (we come back to this in the next section) and since then financial performance has been well below the pre-COVID period. As the charts show, gross margin is trending lower, SG&A costs are trending higher and the company has spent a lot of capex dollars opening new stores into a soft operating environment.

These trends are leading to estimated EBITDA for FY2024 of $24mm, the lowest in the company’s history and a paltry 1.9% margin. SPWH’s former CEO, Jon Barker, left in 2023 and after a long search they recently hired a new CEO, Paul Stone. Judging solely by the numbers, it is our view that Mr. Barker did a poor job managing SPWH.

We do not yet know Mr. Stone’s plan for turning around the company but at least he indicated SPWH will not open new stores in calendar 2024. Gross margin was pre-announced lower for 4Q so we assume (hope) their inventory position was reduced to improve liquidity as the company was carrying an excessive 183 days [(inventory/LTM cost of goods)*365] worth of stock.

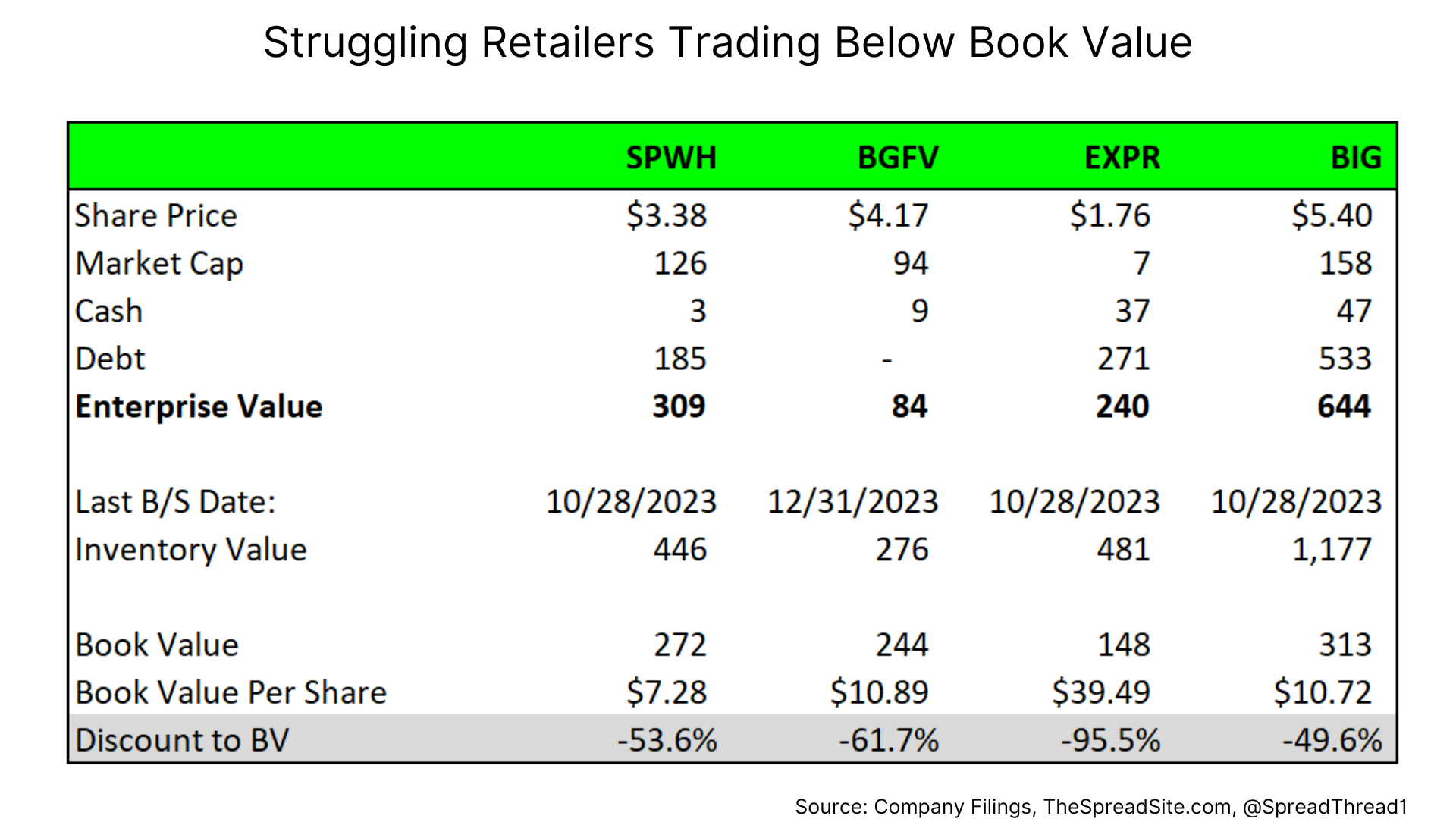

With shares hitting all-time lows, some have highlighted the company is trading below book value. This is true, however, most of that value is inventory with a questionable recovery in a true liquidation. Further, SPWH isn’t the only struggling retailer where this is the case.

Therefore, we don’t put much credence in a retailer trading below book value. On next year’s EBITDA, SPWH is trading at 6.7x, hardly ‘cheap’ for a struggling retailer.

With respect to liquidity, SPWH has a $350mm asset based revolving line of credit “ABL” maturing in 2027 with availability as of FY3Q24 of $111mm. As is common in retail, these lines of credit provide advance rates based off a formulaic calculation whereby the company borrows against inventory and receivables. The issue with ABL facilities is they do not provide much flexibility for a retailer with declining revenue and gross margin as the borrowing base starts shrinking.

Moreover, if suppliers start getting nervous, they demand faster payment which further reduces liquidity. For example, as of FY3Q24, SPWH had $83mm of payables outstanding at ~34 days average payment terms [($83mm/LTM COGS)*365]. If suppliers demanded payment in 5 days, for instance, it would be difficult for SPWH to fund this reduction in working capital with current liquidity.

Attempted Buyout by Great Outdoors, LLC

As mentioned, in late 2020, SPWH received a buyout offer from Great Outdoors, LLC at $18/share and then a year later the deal was terminated after the FTC indicatated they would not sign off on the deal without major store divestitures (SPWH received a $55mm termination fee).

What we find interesting about the attempted buyout is that SPWH was first approached in January 2020 when the share price was around $6.00. Even assuming a large premium (let’s say $7.50), a deal at that time would have been well below the formal bid of $18.00 (a $500mm EV at $7.50 vs $800mm at $18.00). In short, we think Great Outdoors realized they were overpaying, were given a way out, but may still want to own the business.

Where Things Could Get Interesting

Assuming SPWH’s situation doesn’t improve organically, we think two scenarios would occur:

- They would seek outside financing likely in the form of senior equity given limited hard assets to borrow against

- They would be forced to file ch.11

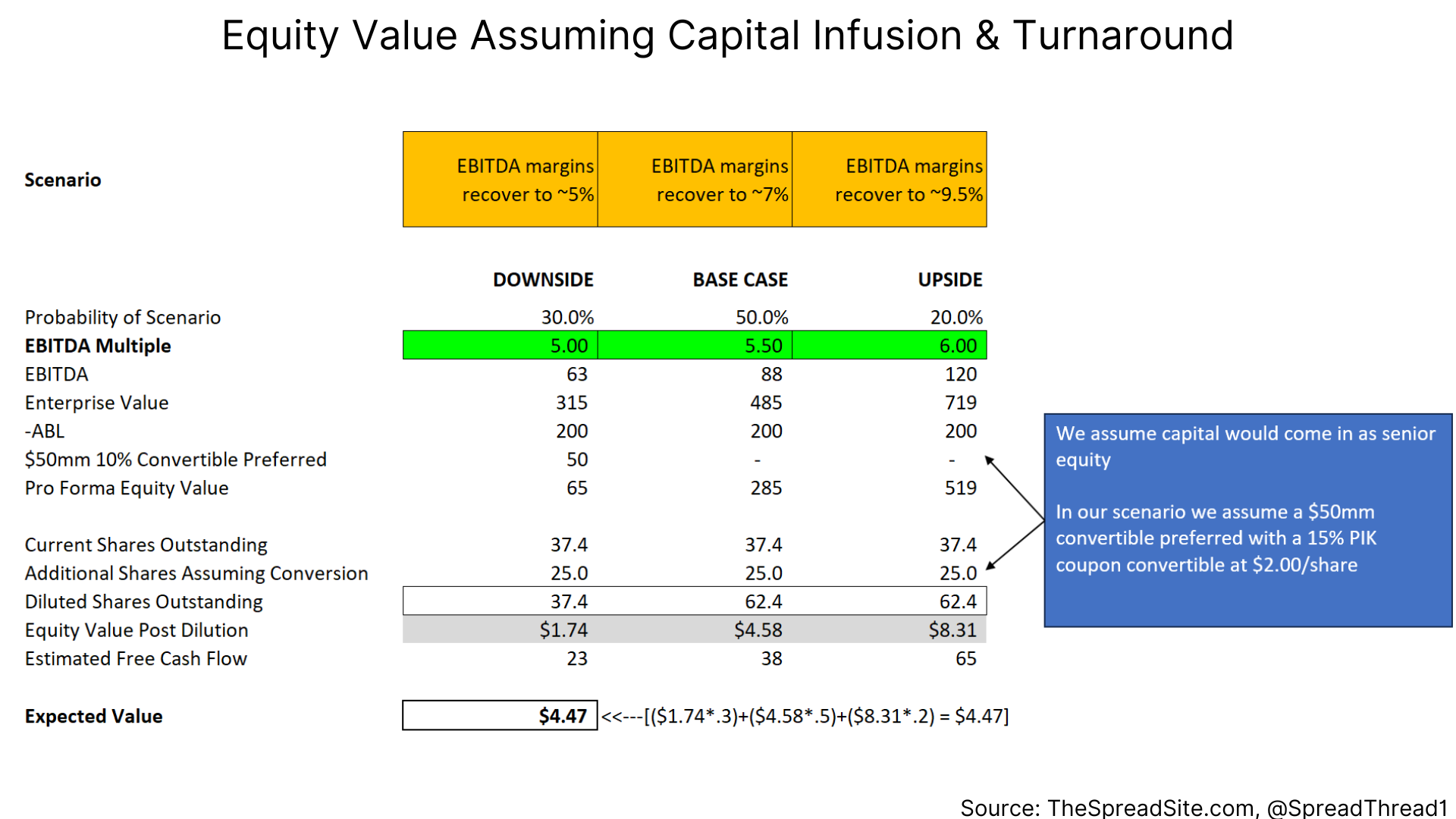

To illustrate equity values in scenario 1, we estimate a $50mm convertible preferred with a 15% coupon (likely in PIK interest) and a $2.00/share conversion price. $50mm of capital could go a long way towards shoring up working capital, paying for restructuring costs and potentially closing underperforming stores. We show three scenarios below with varying levels of EBITDA.

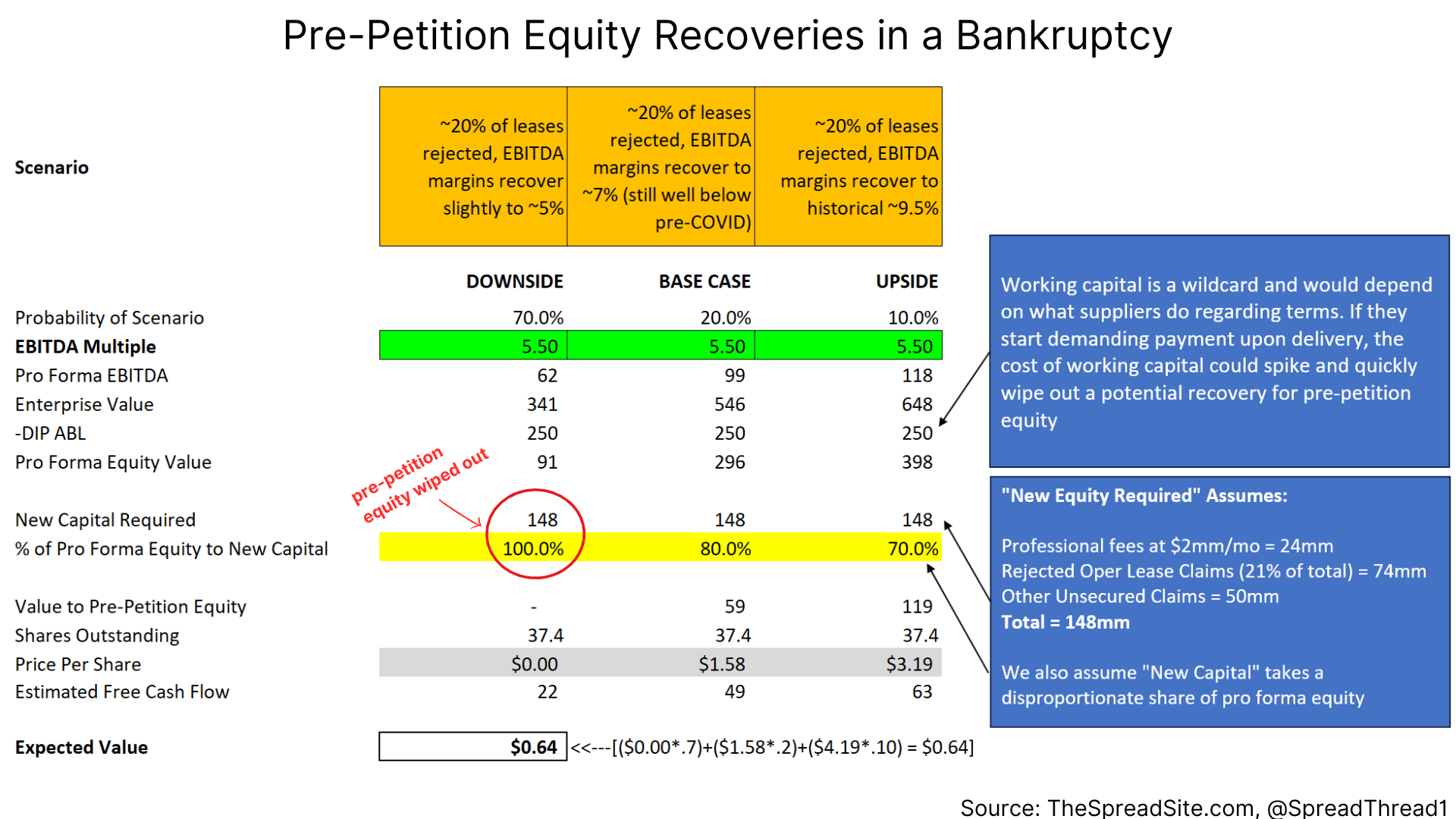

In Scenario 2, we think it is possible Great Outdoors could come back to the table and try to acquire the company as they would be able to simply reject leases on stores they didn’t want or in geographies where the FTC had issues over competition. This situation is much more complicated for pre-petition equity as we think any buyer of the company (Great Outdoors or a financial buyer) would be in the driver’s seat as the liquidity provider and likely require 100% of the equity as compensation.

However, given some hedge fund ownership of SPWH equity we think an Equity Committee would form and fight for some amount of recovery. In other words, we don’t think it is a foregone conclusion that the equity would get wiped out in a bankruptcy. Our assumptions under Scenario 2 are below:

As to the question of why anyone would want to provide capital to SPWH or buy them outright (aside from a strategic), we have a few thoughts:

- SPWH serves a niche (gun sales) where competitors are leaving rather than entering the space

- We assume the business was poorly managed and don’t see why a return to a 7 to 10% EBITDA margin isn’t possible through a restructuring

- Assuming low growth and improved margins, SPWH should be able to convert ~40-50% of EBITDA to free cash flow

We are monitoring SPWH's performance and should the equity continue to trade lower it could offer an interesting opportunity on a distressed situation.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}