Spirit (Airlines) in the Sky

Summary

- We believe the Spirit/JetBlue merger is dead and leaves Spirit facing tough industry fundamentals along with a large $1.1b debt maturity in 2025. Capacity in the domestic air travel market is outpacing demand and rising operating costs are outpacing price increases.

- Spirit (and airlines generally) are incredibly sensitive to minor changes in pricing, capacity utilization and costs. There is significant upside to EBITDA should operating conditions turn around, but structurally, the airline business remains a very difficult way to generate long-term returns. Airline equities are trading vehicles at best, in our view.

- Spirit stock could return to ~$16-$21 assuming an upside scenario we discuss below (but the downside is a zero in bankruptcy). Other airline equities have similar upside while taking substantially less liquidity and bankruptcy risk. Probability weighted and given our macro views, we do not think now is the time to own domestic airline equities, and view Spirit’s 8% ’25 secured notes and convertible bonds as relatively more attractive than the equity at ~$6.30, on a risk adjusted basis.

Introduction & Brief Airline Industry Overview

Hopefully the Norman Greenbaum “Spirit in the Sky” reference came through (great song in case you are not familiar) and adds levity to the Spirit Airlines saga. After all, only an airline can be caught in a bidding war one year and fend off bankruptcy chatter the next. But that is exactly where Spirit Airlines (“SAVE”) finds itself.

In this report we discuss general information on the airline industry, the background of JetBlue and Frontier’s fight to acquire SAVE, and the current state of Spirit’s operations and outlook.

Airlines are among the most cyclical, high fixed cost, and commoditized industries on earth while being littered with bankruptcies and consolidation. The sector can be broken down into three categories (focusing only on US operators):

- Legacy Carriers: Large companies like United and Delta that fly domestically as well as internationally with higher cost structures given their network setup and generally more complex business models. Legacy carriers have a much larger mix of international flights and cater to the highly profitable business customer.

- Low-Cost Carriers ("LCCs"): Southwest pioneered this market flying only domestically on point-to-point routes with a single type of aircraft. Some carriers offer short international flights, but generally these are domestic airlines with lower cost structures and a more pared down flight experience.

- Ultra Low-Cost Carriers ("ULCCs"): This is where Spirit fits and is the lowest cost category with fares that generally undercut the competition. These carriers have cramped aircraft and charge extra fees for basically everything.

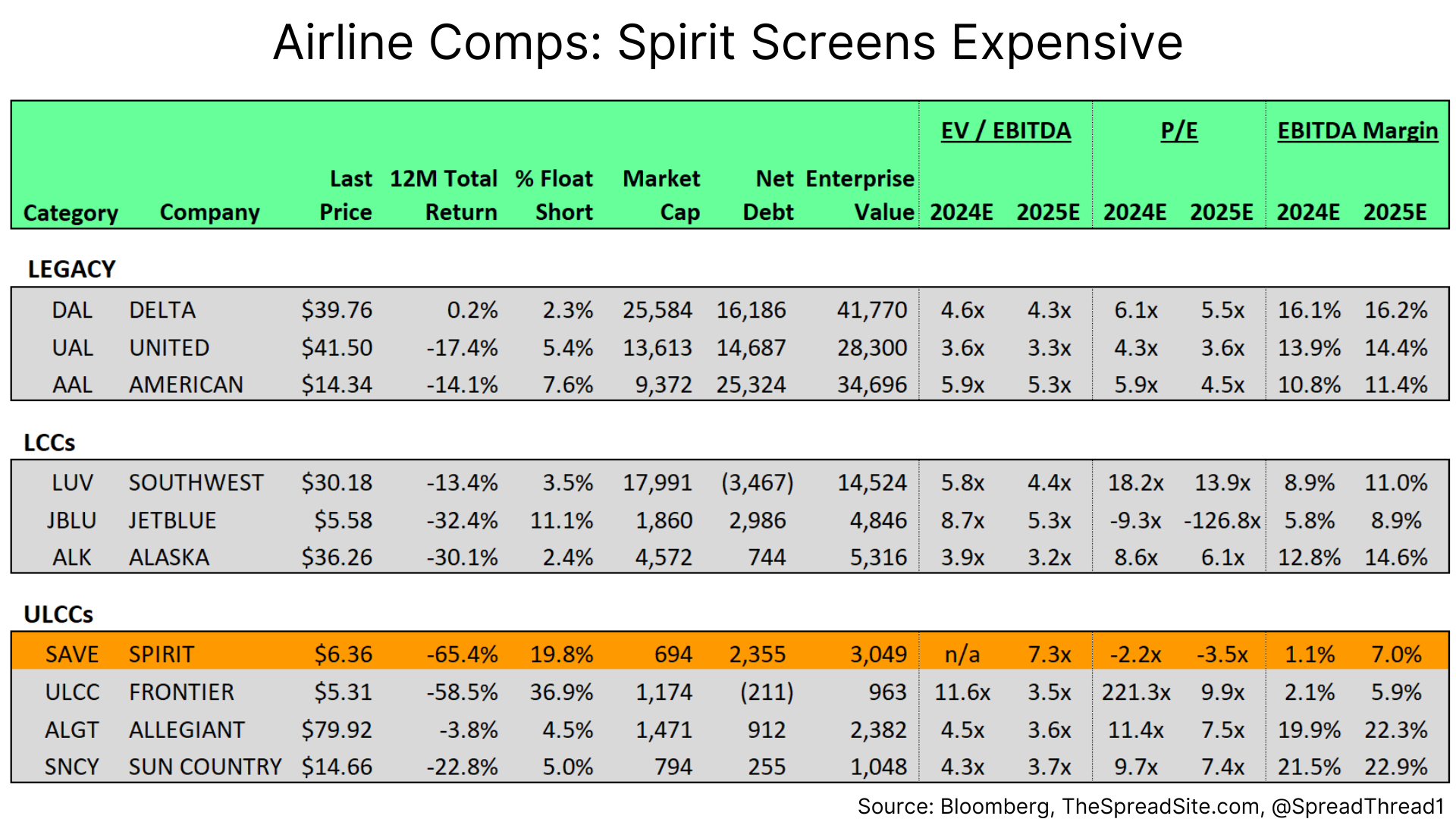

Side Note on Comp Valuation

Airlines are typically valued using EV/EBITDAR whereby aircraft rent is added back to EBITDA and operating leases are capitalized as debt. However, we cannot see detailed estimate breakdowns in Bloomberg, so we use EV/EBITDA. Additionally, estimates for Spirit are all over the place given the recent deal break and we make some assumptions & adjustments above. However, we note that across the board, Spirit trades at a minimum of two turns higher than peers.

Carriers such as Southwest and Alaska try to differentiate themselves with friendly service, but consumers generally do not care which airline they fly, only the price of their seat, causing extreme price competition. With very high fixed costs (i.e. owning and operating a fleet of aircraft and terminals), operational leverage is extreme as the marginal cost of an extra passenger is very low. This is why in “good times” airlines generate huge amounts of cash flow. On the flip side, it is quite easy to bring on new capacity (especially given the robust aircraft finance market) and in “bad times” airlines will compete to zero (or negative) profitability. Simply stated, airlines are willing to sell tickets at an EBITDA loss if it helps cover fixed costs.

Background on Frontier / JetBlue / Spirit

In February 2022, Frontier Airlines (“ULCC”) announced plans to acquire Spirit for roughly $6.6b through a combination of cash and stock with an expected closing date in 2H22. In April 2022, JetBlue (“JBLU”) presented an all-cash offer to acquire Spirit for $7.3b, which Spirit rejected given regulatory concerns and entered into an agreement with Frontier. Ultimately, JetBlue sweetened their terms to $33.50/share in cash (~$7.6b EV) and Spirit terminated their deal with Frontier while agreeing to be acquired by JetBlue as of 7/28/22.

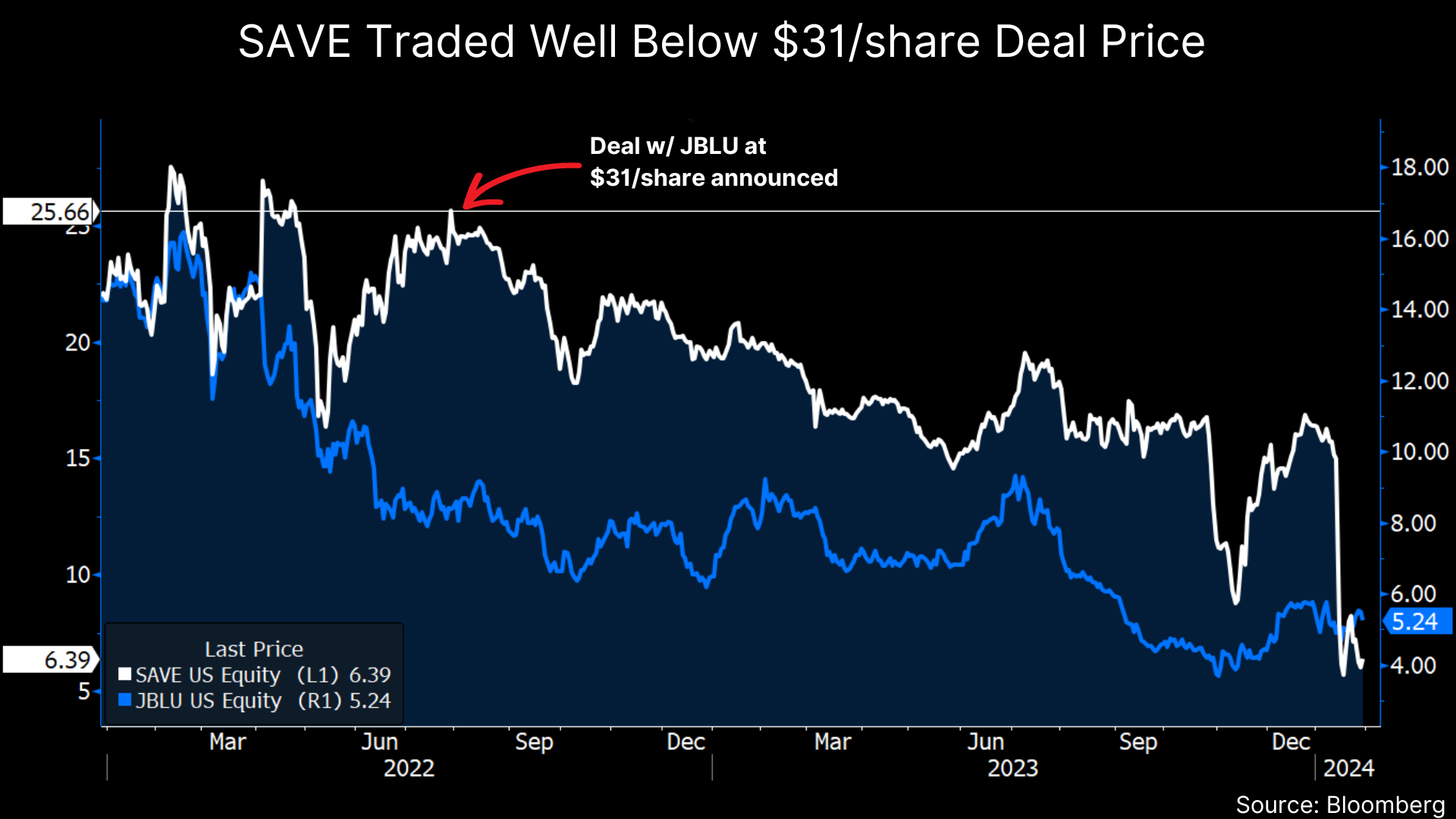

There are some nuances to the per share consideration, but Spirit shareholders received $2.50 upfront (on 10/26/22), plus a $0.10/month “ticking” fee while the deal was going through standard closing conditions. If the deal closed, Spirit shareholders would have received $31/share in cash for a maximum consideration of $34.15 (depending on ultimate closing date).

The market placed substantial risk on the SAVE/JBLU deal going through on original terms as SAVE stock never traded close to the $31/share deal price.

And rightly so because on 3/7/23 the DOJ sued to block the merger on antitrust grounds and as of 1/16/24 won an injunction from the District Court of Massachusetts blocking the two companies from merging. Per the merger agreement, JBLU is required to appeal but has a low probability of success. In our view (and most of the market), the merger is dead and JetBlue will end up paying another $70mm to Spirit given the deal failed to close on antitrust grounds.

Historically, airline mergers allowed carriers to reduce cost and excess capacity but with the recent DOJ win, further M&A faces an uphill battle (note that Alaska Air is working to close a deal to acquire Hawaiian Air for $930mm).

Quick Sidebar on Key Industry Operating Metrics

We reference these terms in the sections below

Revenue Passenger Miles ("RPM"): The number of miles travelled by paying passengers in a period.

Available Seat Miles ("ASM"): The total number of miles flown by an airline in a period based on total capacity of all aircraft in their fleet.

Load Factor: A measure of how full aircraft are during a period, calculated as RPM / ASM.

Yield: Shown on a per mile basis, this metric illustrates the average ticket price received by airlines from passengers. The calculation is Revenue / RPM. When industry analysts talk about pricing, they are usually referring to Yield.

Passenger Revenue per ASM ("PRASM"): This is [Yield * Load Factor] and provides a metric for revenue per mile while incorporating capacity utilization.

Cost per ASM ex Fuel ("CASM ex Fuel"): This metric represents total operating costs (excluding fuel) per ASM and is useful to compare cost structures across different airlines. (“CASM”) represents all costs on a per mile basis, including fuel.

Spirit Airlines Standalone

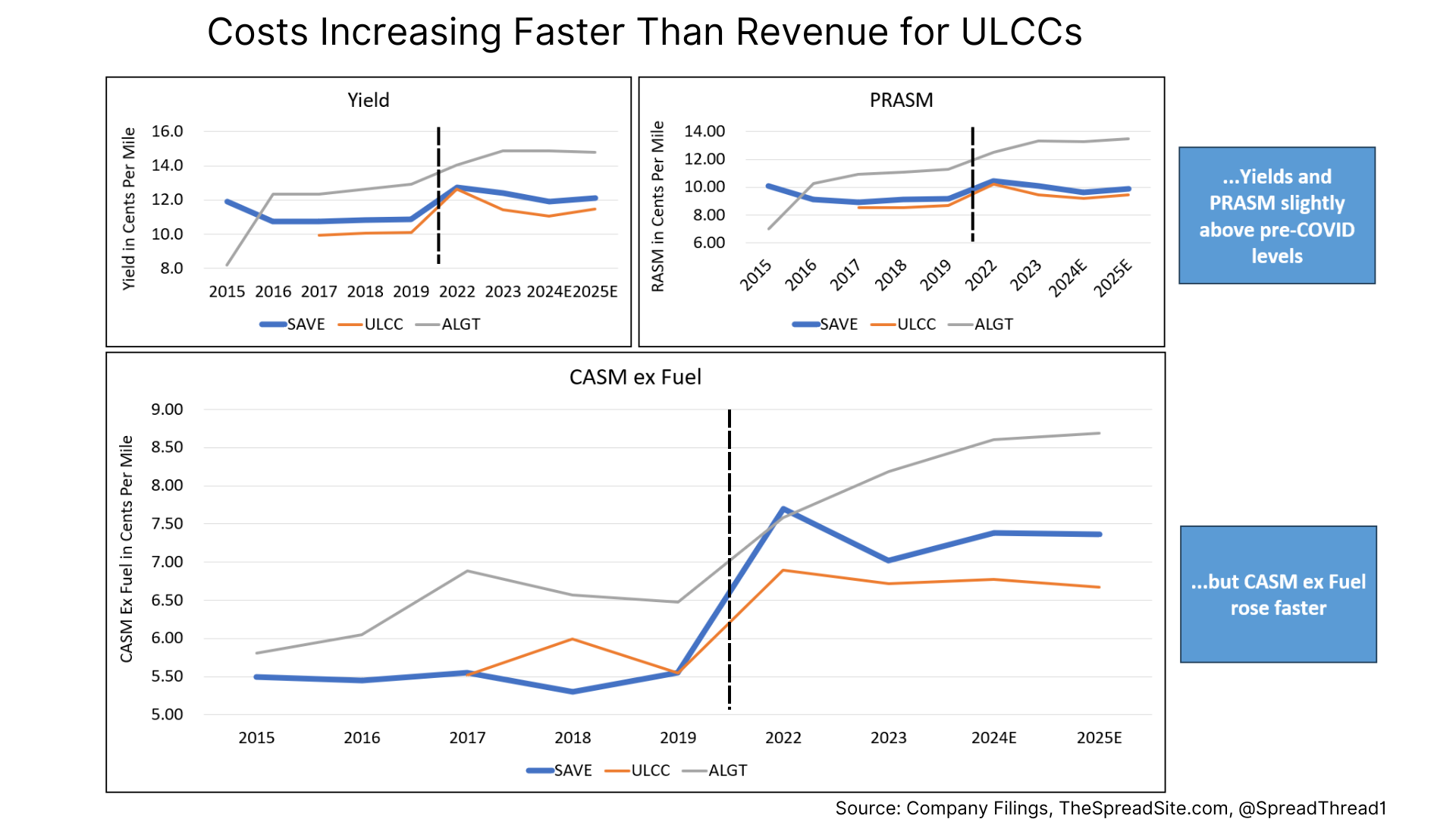

Without a merger partner, Spirit now faces a weak domestic travel market and elevated costs. International travel remains strong, but domestic capacity growth is outpacing demand with a ~9% increase in 2023 and another 5 to 7% expected in 2024. Post COVID, inflationary cost pressures have outpaced fare increases for the ULCC carriers as shown below (dotted line bifurcates pre and post COVID).

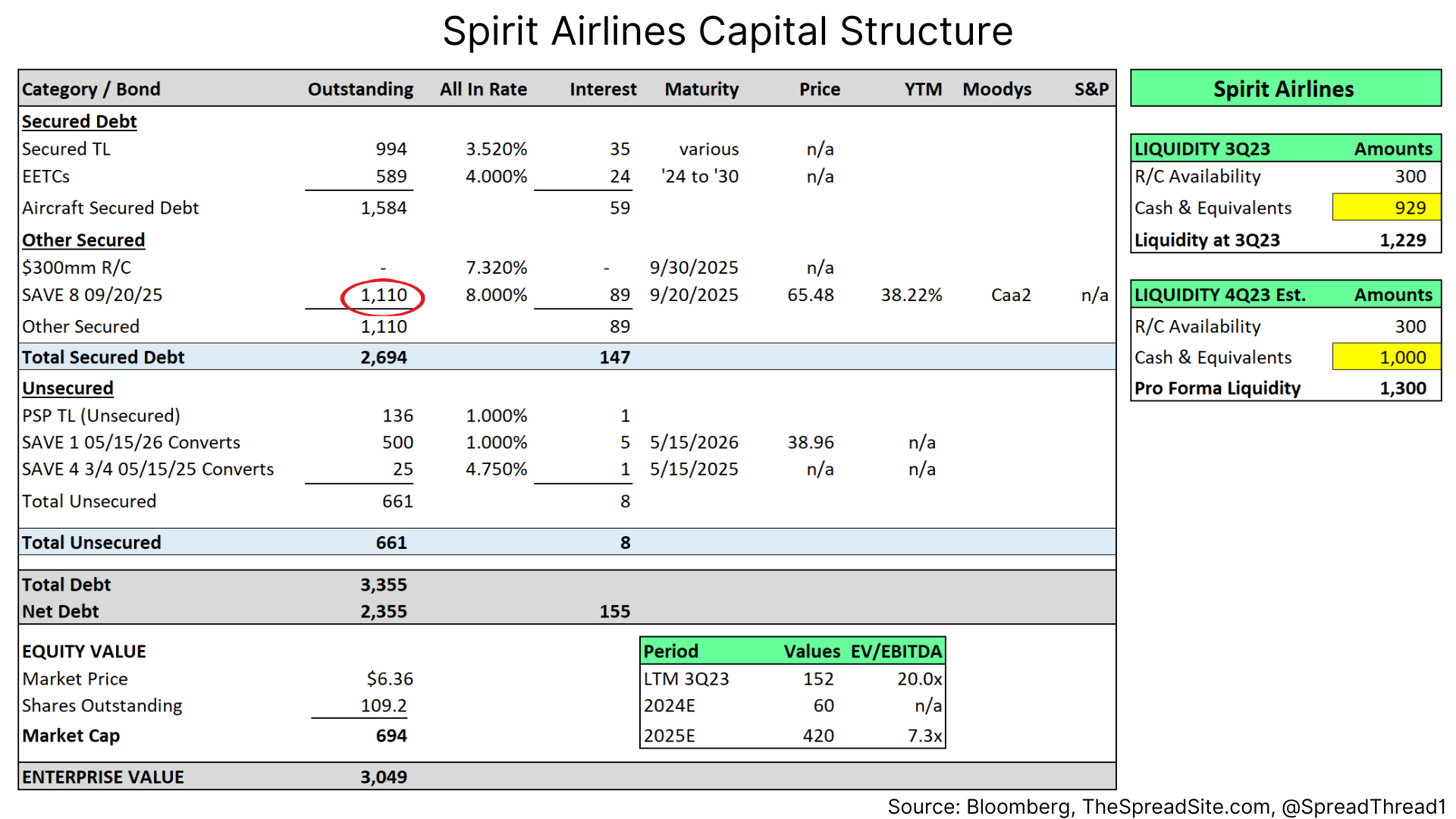

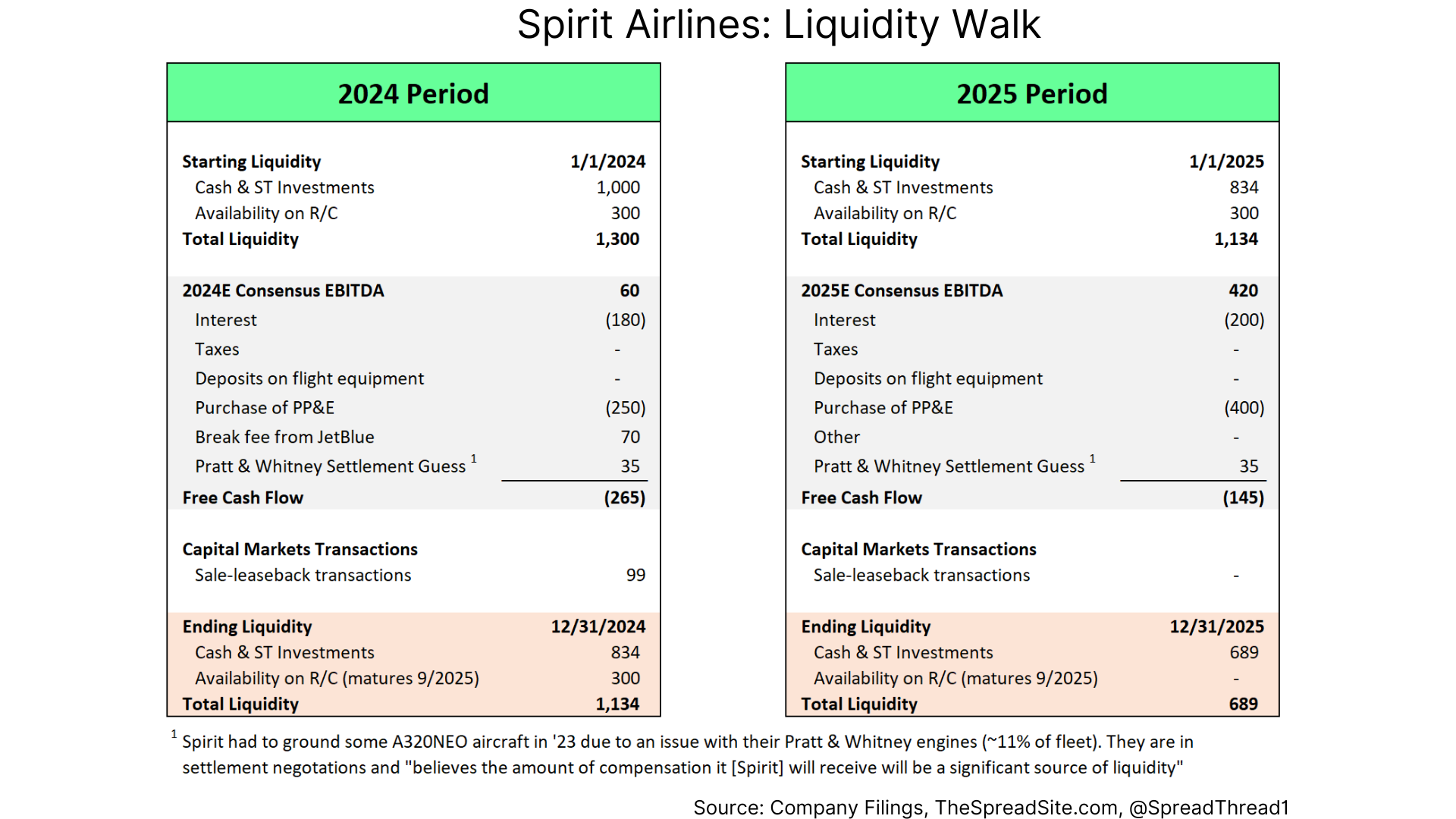

With the backdrop of weak fundamentals, Spirit also faces a $1.1b bond maturity due on 9/2025 (red circle in image below) currently trading in the mid-60s. Since the JBLU deal break, this bond maturity caused rumors to swirl that Spirit may need to restructure if conditions don’t improve.

Barring a large turnaround in fundamentals, Spirit will not be able to repay their 2025 debt maturity with liquidity on-hand as shown by our “liquidity walk” which uses consensus estimates to pro-forma liquidity through 2025. This doesn't automatically mean the maturity will force bankruptcy, only that they won't have enough cash on hand to repay it.

Capex for new aircraft is a wildcard as Spirit has aircraft purchase commitments of $454mm in 2024 and $1b in 2025. These deliveries will require at least partial secured financing and any delays should help given weak industry fundamentals.

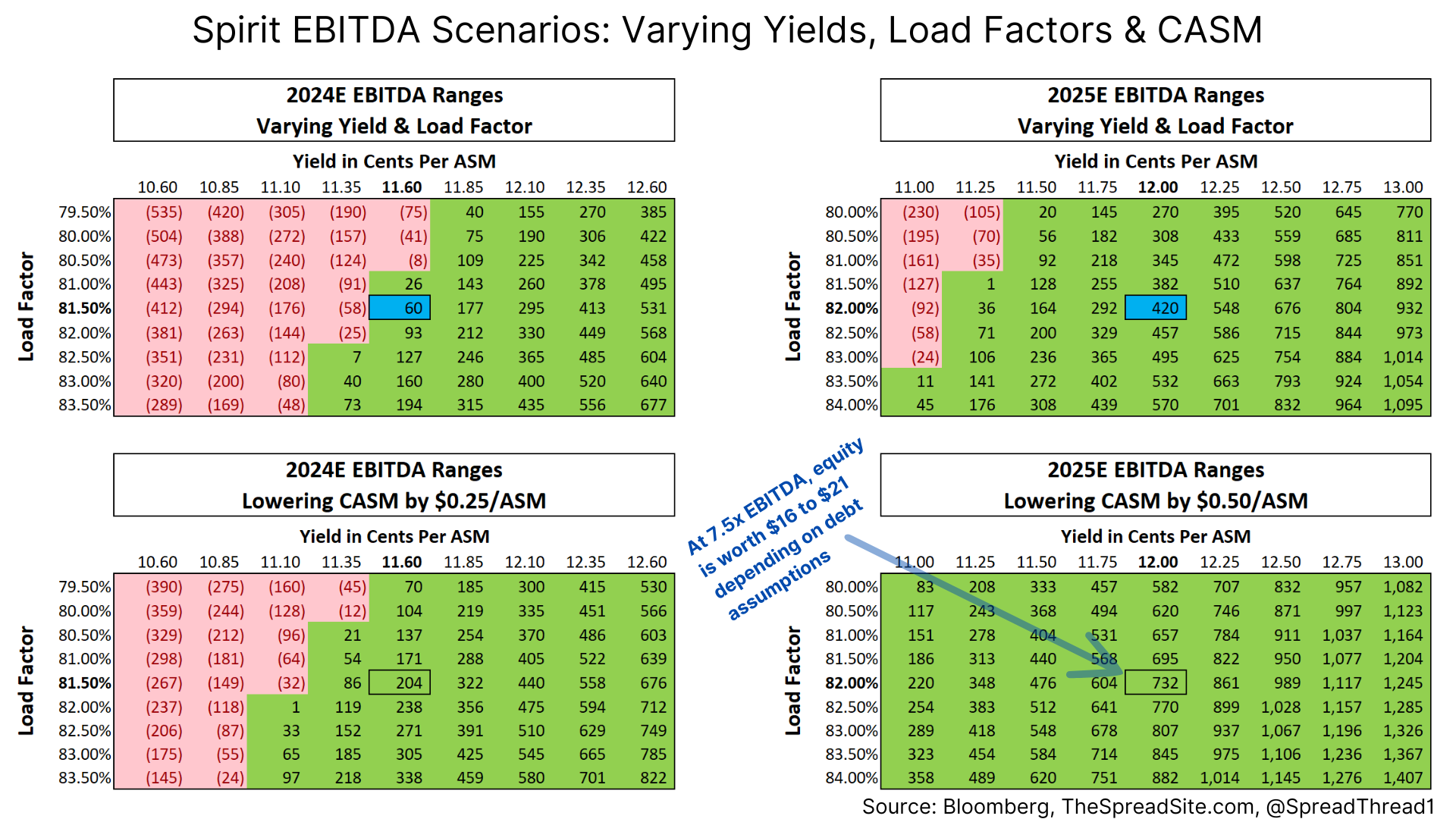

Spirit will certainly attempt to raise additional capital and reduce costs. As of 9/30/23 they had 22 unencumbered aircraft and could do additional sale-leaseback transactions. On the cost side, it is unclear where opportunities lie but we note their CASM ex Fuel is above Frontier’s (pre-COVID it was below), so perhaps they have room to cut. Separately, fundamentals in the industry could improve. To illustrate just how sensitive airlines are to small changes in operating conditions we show the following sensitivity tables. The top two hold costs (including jet fuel) constant. While the bottom two assume Spirit can lower CASM (including jet fuel) by $0.25/ASM in 2024 and $0.50 in 2025. Granted, this represents a significant cost reduction and may be unrealistic; we just want to show the sensitivities.

Debt & Bankruptcy

As mentioned, not having cash on hand to repay the 8% ’25 debt maturity does not automatically mean Spirit will file ch.11. If industry conditions improve, they could likely refinance this debt or try to do exchange offers with debtholders. While a full restructuring analysis is outside the scope of this report, we will make a few observations on the $1.1b 8% ’25 secured notes:

- This bond is likely the “fulcrum” security, meaning holders of this debt would convert to equity in a bankruptcy.

- While the bond is “secured,” the collateral is a 1st lien on Spirit’s “Free Spirit” loyalty program, which is not worth nearly the $1.1b of debt outstanding. Should Spirit file ch.11, there would be a fight over the value of the collateral and recoveries relative to the $525mm unsecured convertible bonds and the $136mm unsecured Payroll Support Program (“PSP”) debt.

- The 8% secured bond has a minimum $400mm liquidity covenant that could be triggered to the extent fundamentals worsen ahead of the 2025 maturity.

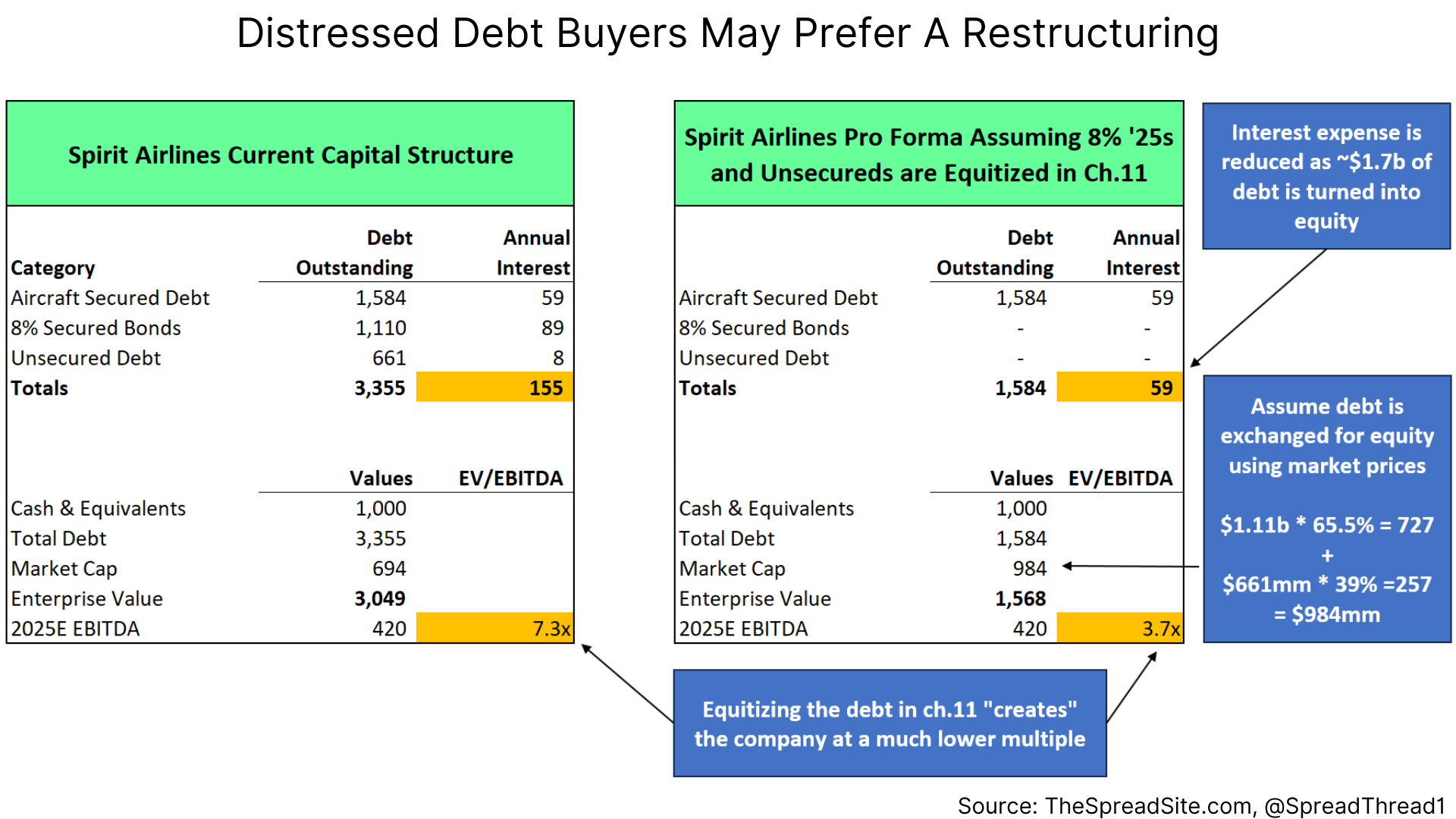

- At a VERY high level, assuming the $1.1b 8% ’25 secured bonds AND unsecured bonds were equitized at current prices, this would leave Spirit with significantly less interest expense and a more attractive capital structure. While an extreme oversimplification, we illustrate that distressed buyers may want to accumulate the 8% ’25 bonds anticipating this debt would turn into equity in a bankruptcy and “create” the company at a much lower valuation than implied by SAVE’s $6.30 share price.

A few other points to note on airline bankruptcies:

- Given the industry’s cyclicality, a 1-2yr bankruptcy could mean a dramatic improvement or worsening of industry conditions. This has significant implications for how securities trade during the restructuring with fights amongst different creditor classes and potential for the pre-petition equity to see a recovery.

- Spirit also has a $1.5b Federal Net Operating Loss (“NOL”) that can be used to offset taxes. While it can be tricky for an acquiror to take over an NOL in bankruptcy, it may have value.

- It may be possible for Frontier Airlines to try and acquire Spirit out of bankruptcy by using a "Failing Firm Defense" as this article from Jones Day describes. We are not experts here, but believe there may be a chance for Frontier to come back if things get much worse for Spirit.

Conclusion

Generally, we are not fond of airline equities. There was a case to be made in 2017 to 2019 that industry consolidation and capacity constraint would finally allow the companies to generate sustainable free cash flow. COVID crushed those dreams and we still view them as trading vehicles, at best.

As for Spirit, we think the equity is a poor relative value compared to the 8% ’25 bonds in the mid-60s, the convertible bonds in the high 30s and relative to other airline equities. With the ‘25E EV/EBITDA valuation ~7.3x vs peers in the mid 3x area and a significant debt maturity in 2025, we think the bonds are a better play, risk adjusted. Assuming the lower right quadrant scenario in our sensitivity analysis plays out, the equity could get back to ~$16 to $21, however, that is not a bet we are comfortable making and believe the risk/reward is more attractive in the debt.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

%20in%20the%20Sky){kind=link}