Front End Corporates

Introduction

Markets surged in the last two months of 2023, leaving investors with few attractive options to start 2024. Stocks are off to a bumpy start after the first few days of the year, but still just off all-time highs. Bonds, where we had been bullish, are also less compelling today with yields almost 100bp below October peaks. Even sitting in cash is “riskier” now (i.e., re-investment risk) with the potential for rate cuts to begin in 1H24. As a result, investors are left asking where to invest excess funds.

Within fixed income, we think it makes sense to move back to the front-end of the curve, given less attractive yields in the long end. We would stick with credits that can easily withstand a downturn, in case markets shift away from the recent ‘goldilocks’ narrative. Yes, you are not going to get rich from front-end BB/BBB bonds, but given the various cross-winds, we like clipping a 5-6% yield in this part of the market until better opportunities arise. In the report that follows, we present 10 ideas along these lines.

Background

There was a time when I was tasked with investing excess cash held within the family office segment of my former company. The mandate was to earn a spread above cash (zero at the time) while keeping a maturity profile of around 2 years. Of course, one could just buy A rated bonds with essentially no credit risk, but in a zero-rate world this meant almost no yield and a questionable level of effort on my end. However, going too low in credit quality to “reach for yield” could mean some sleepless nights, or worse, an actual impairment.

Therefore, the sweet spot was typically in the BB to BBB ratings spectrum with chosen bonds containing one or more of the following criteria:

- Significant liquidity to repay near-term maturities (i.e. not solely relying on refinancing)

- High EBITDA margins or FCF conversion ratios allowing flexibility during downturns

- Large differentials between leverage through the chosen bond and EV/EBITDA (i.e. significant valuation cushion through the debt)

- Limited industry cyclicality and/or tail risks

Using a similar framework, while also controlling for bond liquidity (i.e. larger issue sizes), and a minimum spread of ~80bp, we highlight 10 short duration bonds where we think investors can earn a reasonable spread/yield while taking limited credit risk. On a portfolio basis, these 10 bonds average a 2yr maturity, 122bp of spread, YTM of 5.53% and span 7 sectors. Finally, a sidenote: Closed-end funds claiming to be “short duration” carry significantly more credit risk than we think is appropriate for the strategy - a point we make in our report titled “Classifying Closed End Funds.”

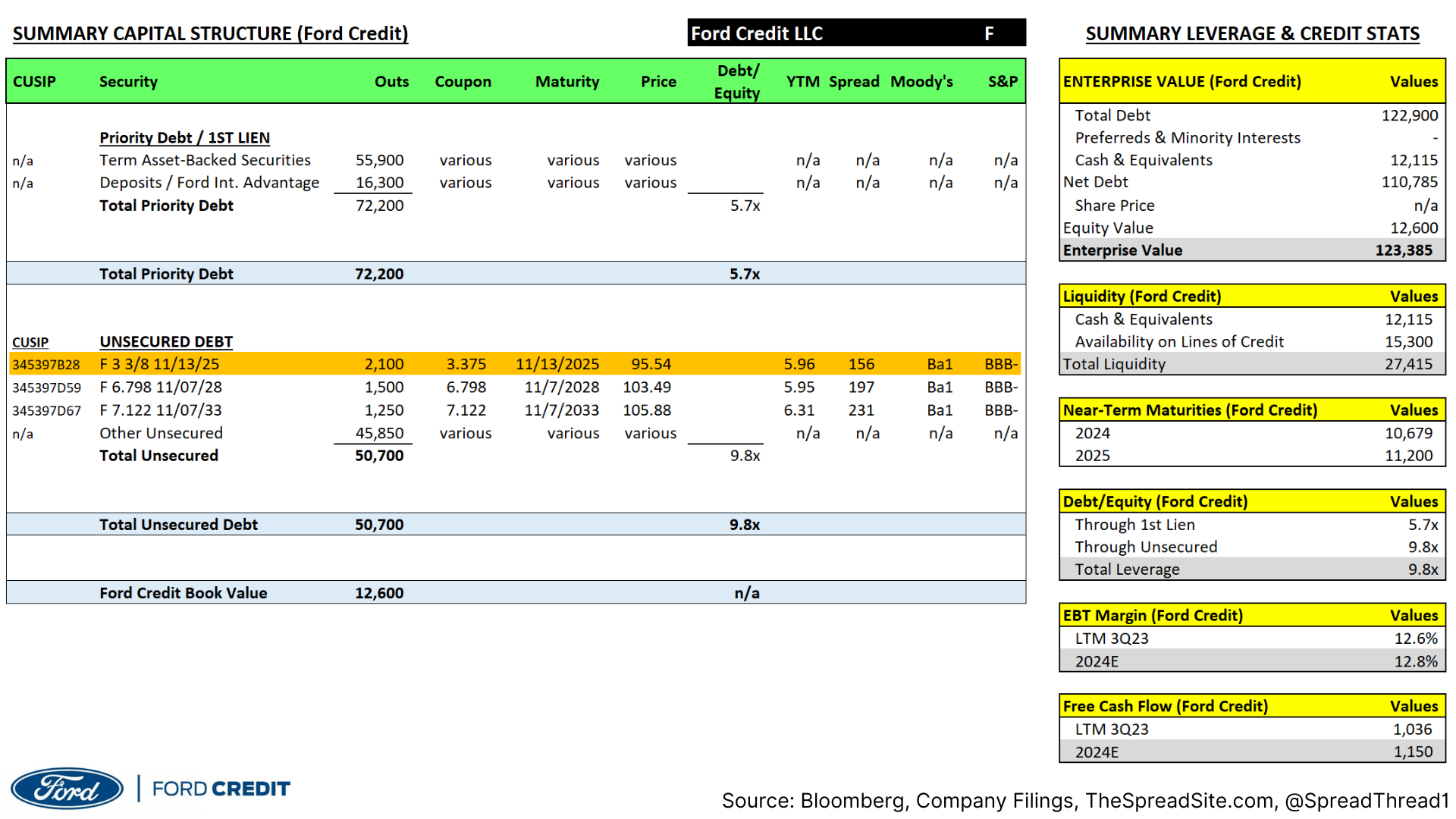

Bond 1: Ford Motor Credit, 3.375% '25

SECTOR: Automotive Finance

156bp Spread, 6.0% YTM

- Positive: Significant liquidity to address near-term maturities

- Positive: Auto loan portfolio primarily to Prime borrowers, very low historical charge offs

- Risk: Relatively larger reliance on financial markets for financing/securitizations

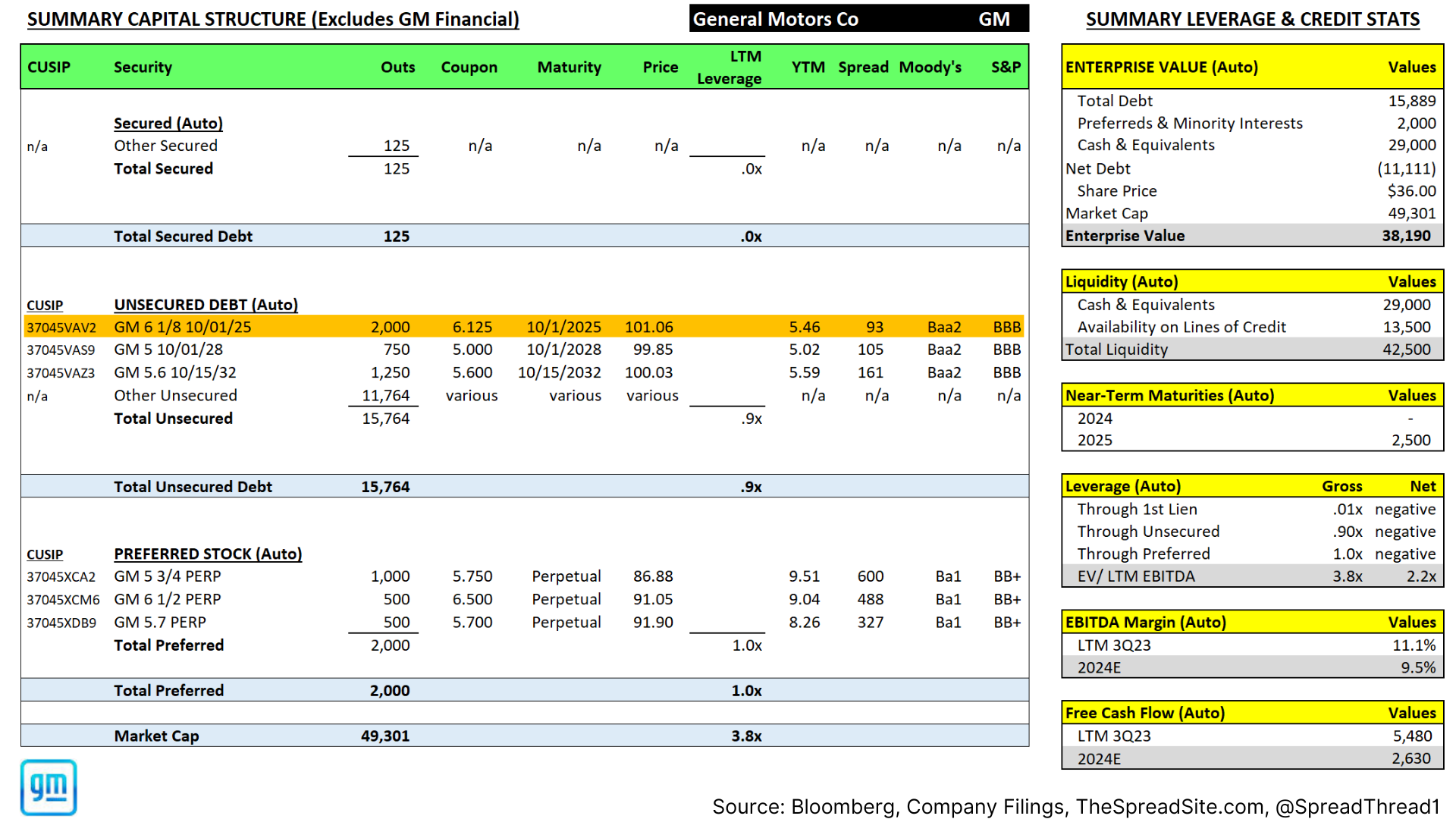

Bond 2: General Motors, 6.125% '25

SECTOR: Automotive Manufacturing

93bp Spread, 5.5% YTM

- Positive: Negative net debt through the automotive manufacturing business

- Positive: Cash on the balance sheet exceeding 2024 and 2025 maturities

- Risk: Very high operating leverage and industry cyclicality

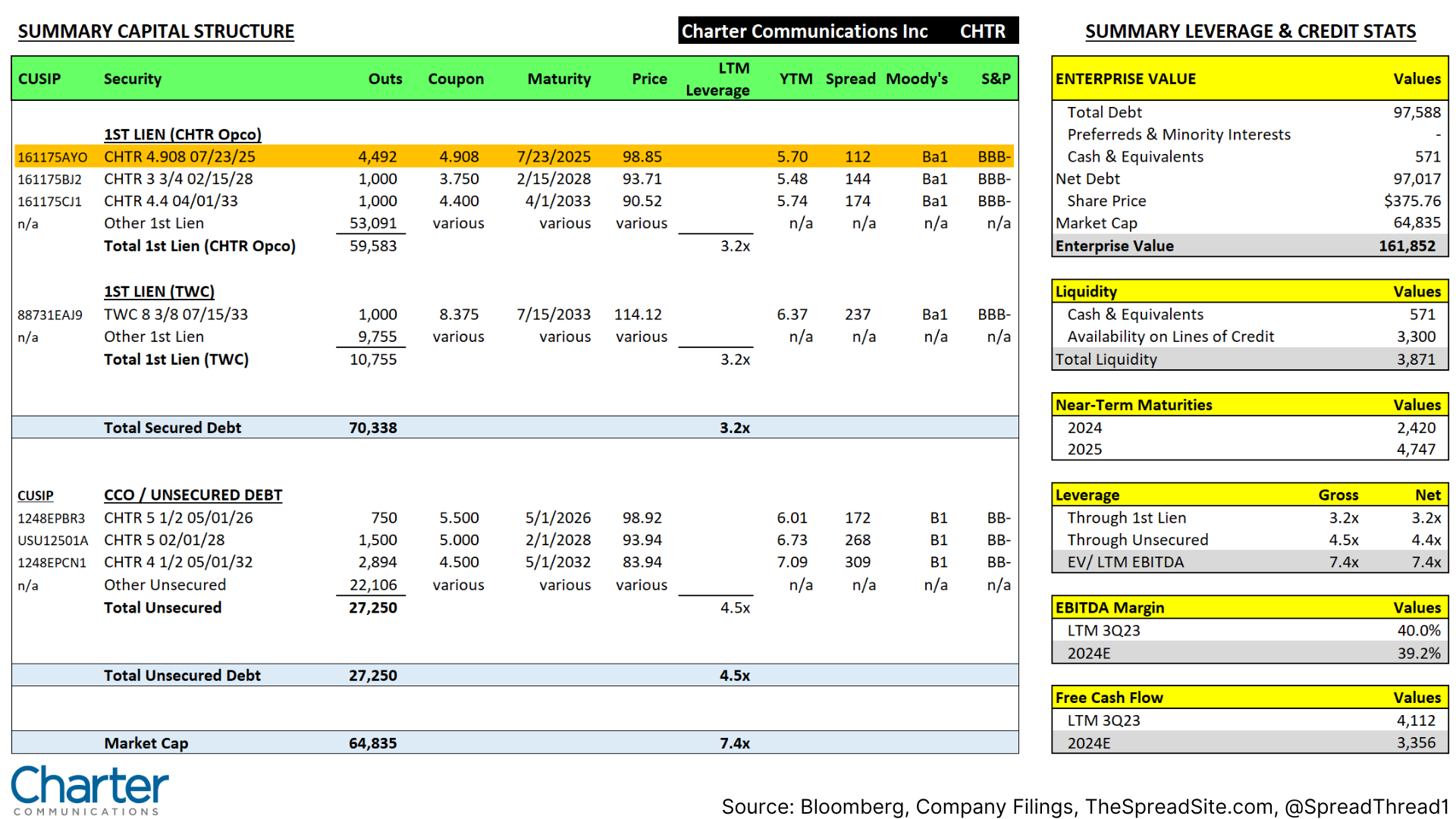

Bond 3: Charter Communications, 4.908% '25

SECTOR: Media

112bp Spread, 5.7% YTM

- Positive: Significant free cash flow expected in the near-term

- Positive: Secured bond, higher in priority relative to unsecureds

- Risk: Some segments (video & phone) are facing long-term decline

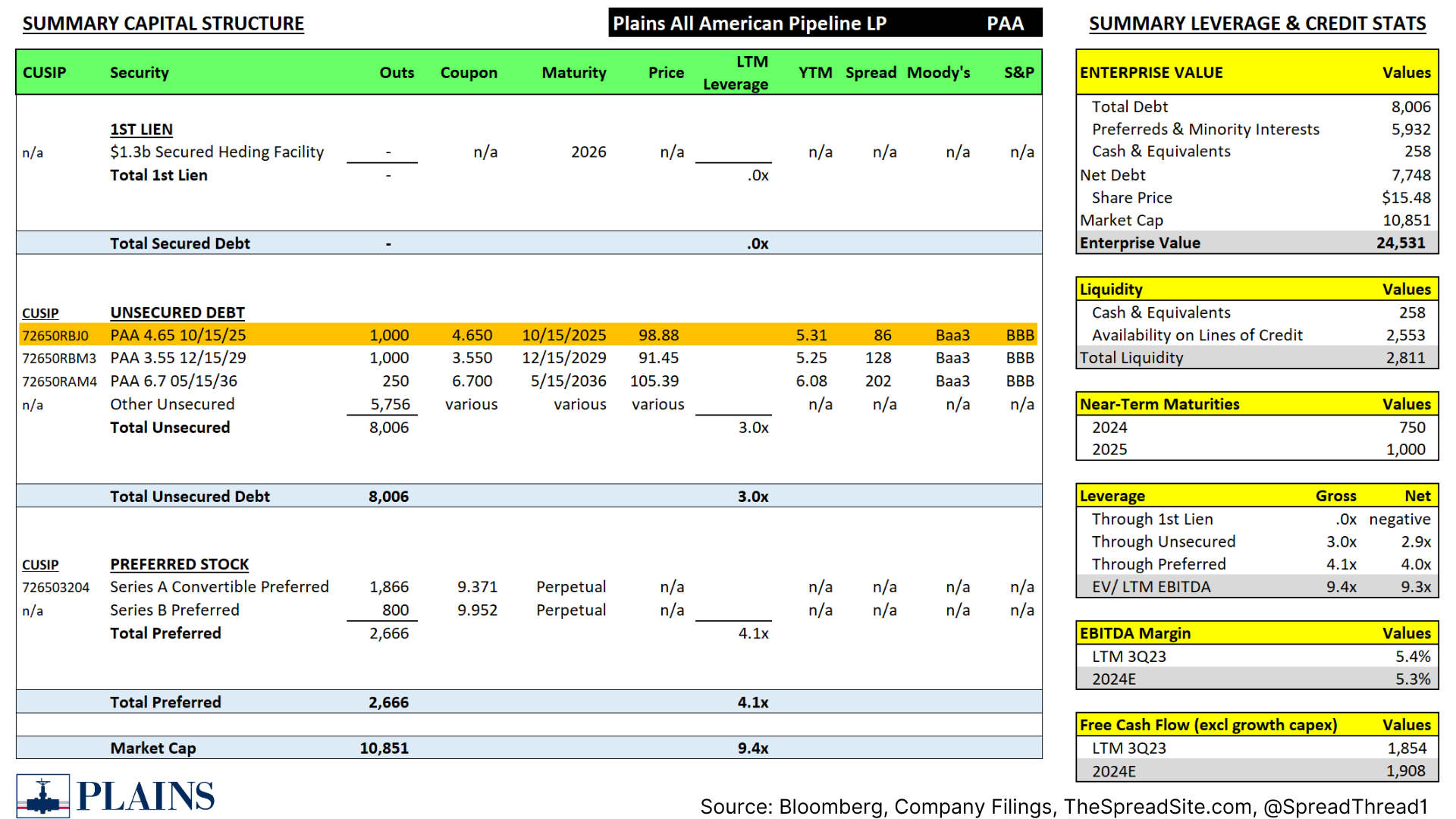

Bond 4: Plains All American, 4.65% '25

SECTOR: Energy (Pipelines)

86bp Spread, 5.3% YTM

- Positive: Large valuation gap between leverage through unsecureds (2.9x net) and EV/EBITDA of 9.2x

- Positive: Significant capex flexibility in a downturn

- Risk: Only ~15% take-or-pay contracts (i.e. more exposure to energy prices)

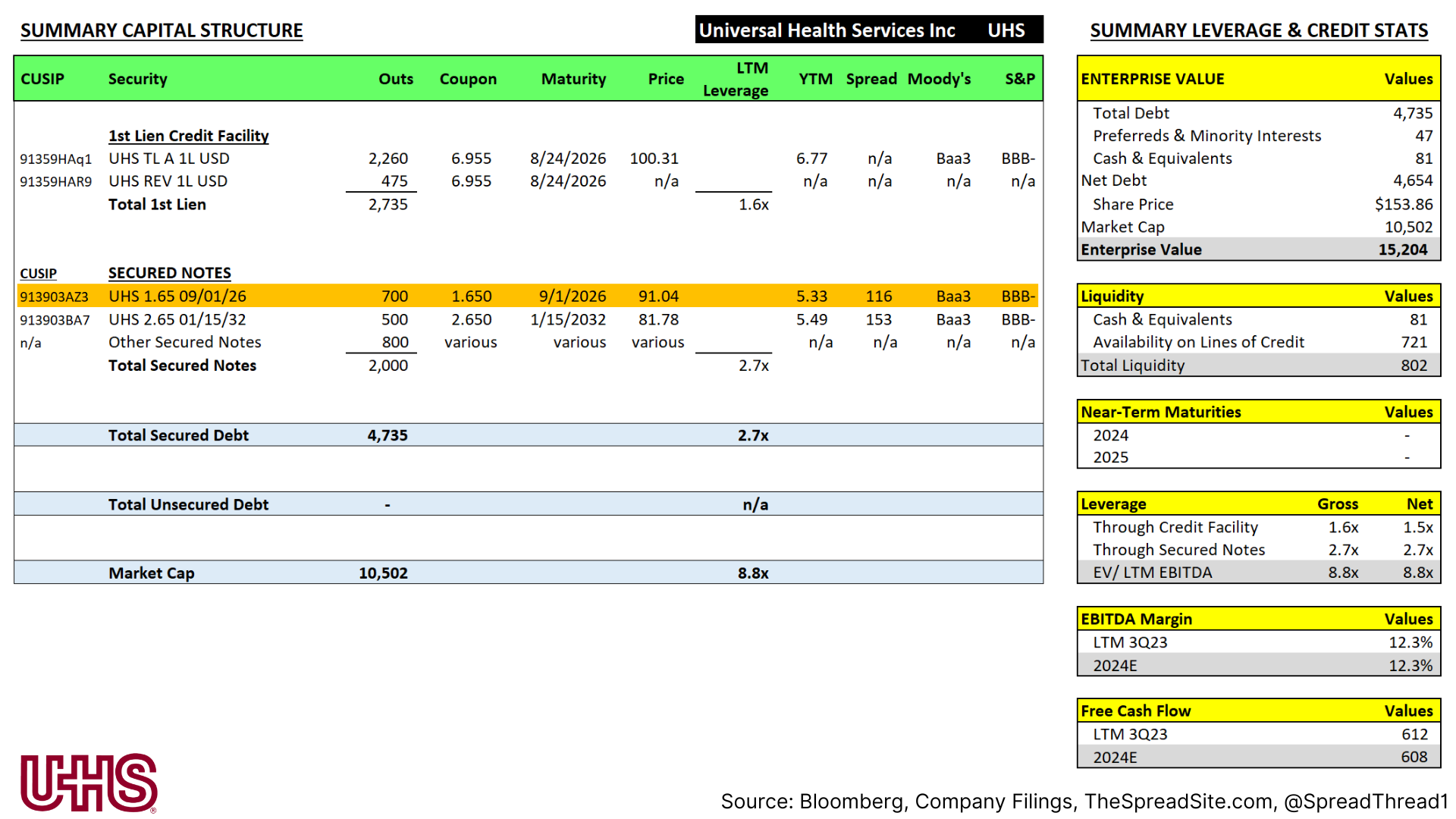

Bond 5: Universal Health Services, 1.65% '26

SECTOR: Healthcare

116bp Spread, 5.3% YTM

- Positive: Large valuation gap between unsecureds (2.7x net) and EV/EBITDA of 8.7x

- Positive: Low overall leverage

- Risk: Large credit facility maturing ahead of bonds

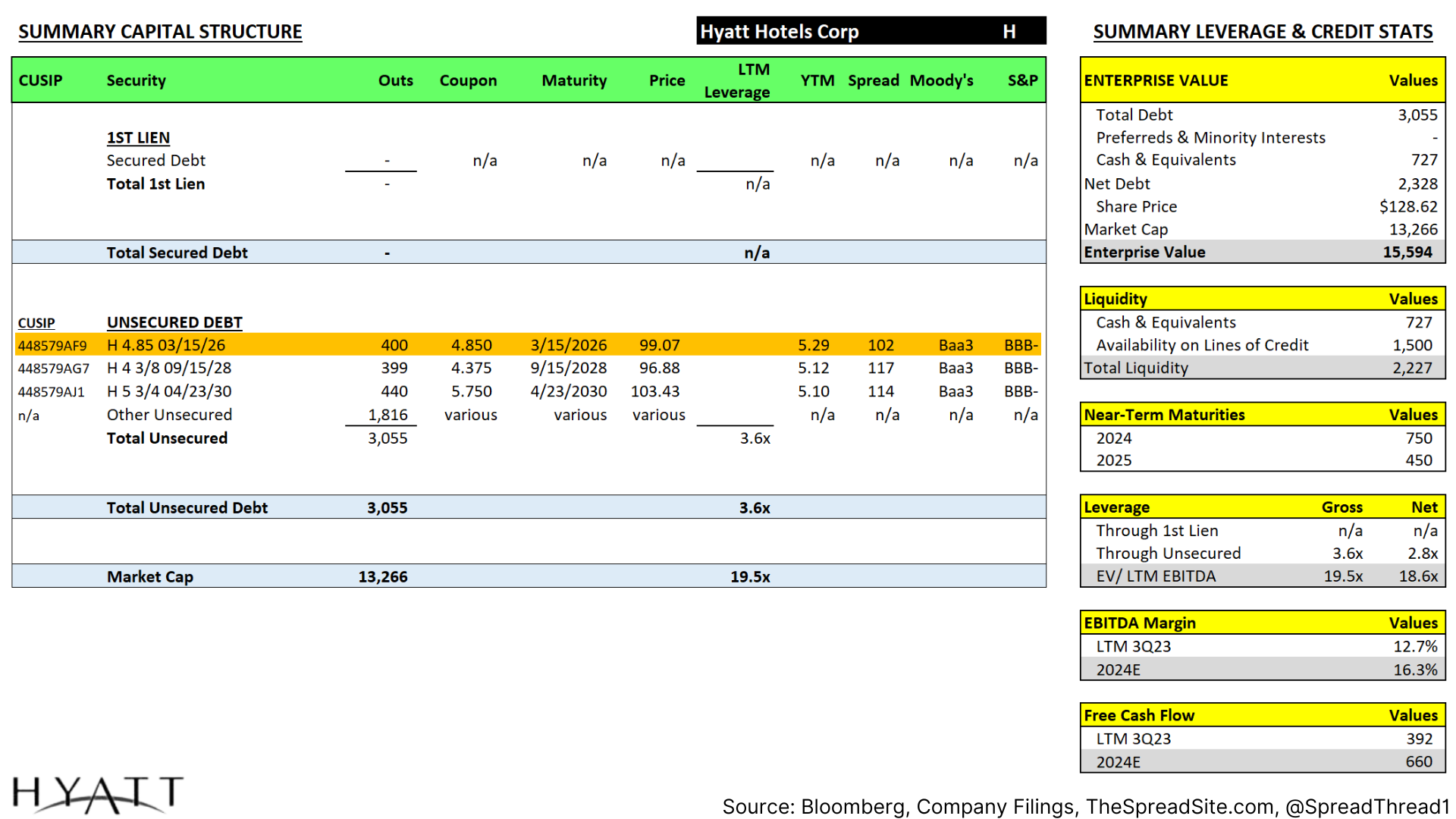

Bond 6: Hyatt Hotels, 4.85% '26

SECTOR: Lodging

102bp Spread, 5.3% YTM

- Positive: Large valuation gap between unsecureds (2.8x net) and EV/EBITDA of 18.8x

- Positive: Low overall leverage

- Risk: Exposure to tail risks impacting all travel and leisure

Note: We are not trying to be vague with the risk factor. In our view, tail risks such as another pandemic, war, terror attacks etc., should be considered when buying short duration credit given its asymmetric risk profile.

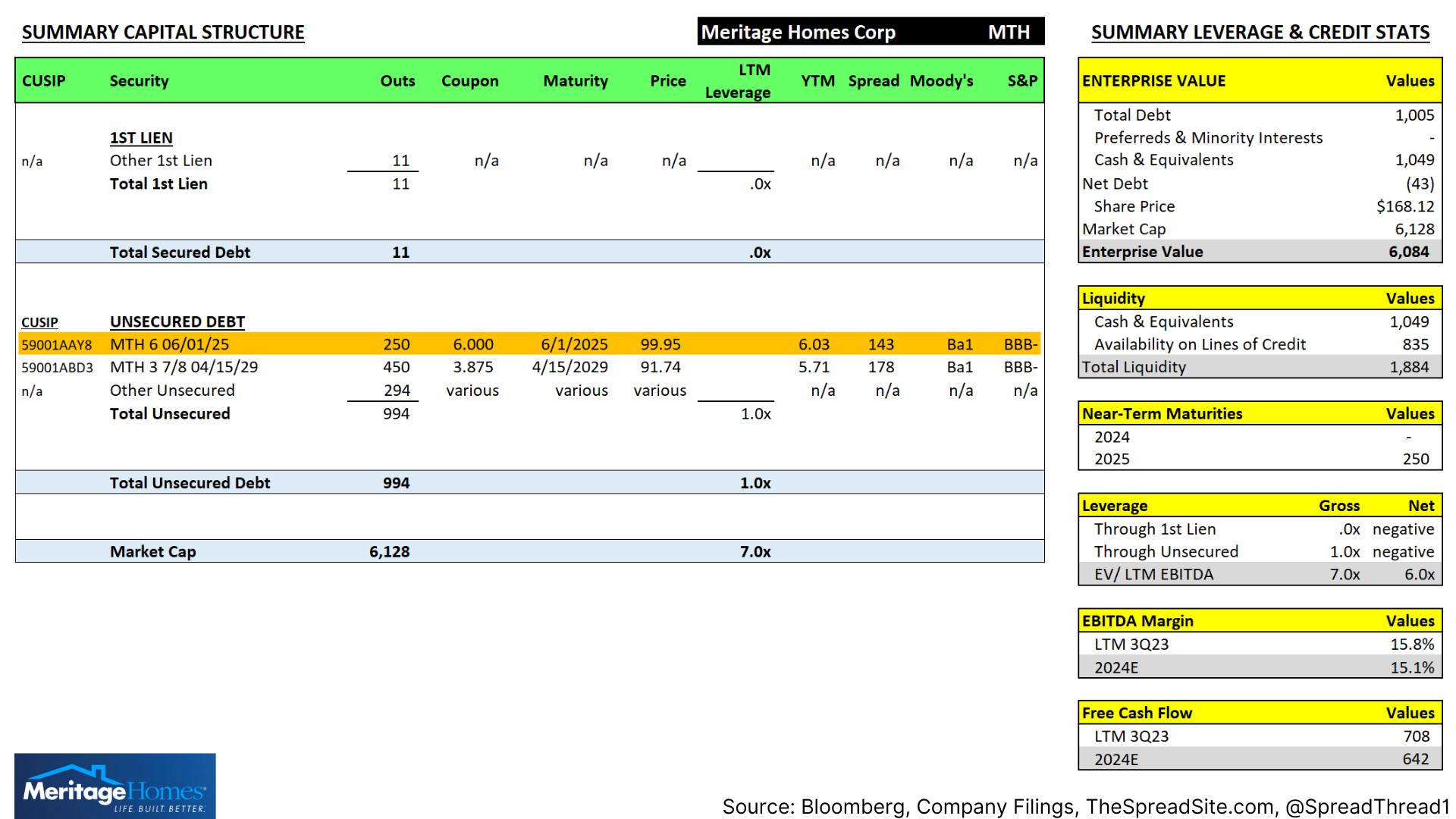

Bond 7: Meritage Homes, 6.0% '25

SECTOR: Homebuilders

143bp Spread, 6.0% YTM

- Positive: Negative leverage through the unsecureds

- Positive: Cash in excess of maturities through 2025

- Risk: Higher than average industry cyclicality

Note: Generally, homebuilders can cut capex to zero in a downturn as they simply stop building new homes. All else equal, we find this is a significant benefit to credit quality and one of the reasons we pick 2 homebuilder credits in this analysis.

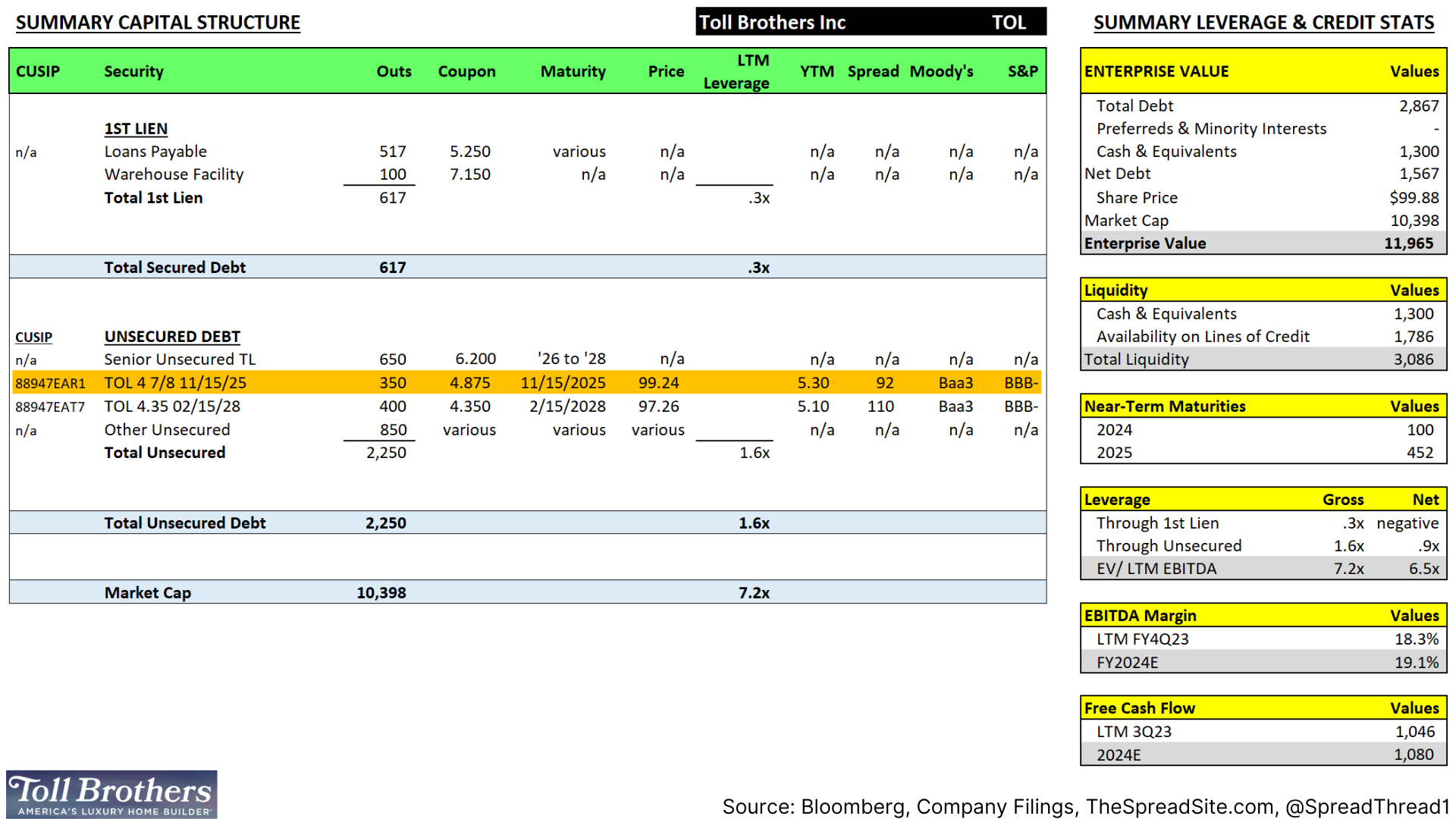

Bond 8: Toll Brothers, 4.875% '25

SECTOR: Homebuilders

92bp Spread, 5.3% YTM

- Positive: Very low leverage through the unsecureds

- Positive: Cash in excess of maturities through 2025

- Risk: Higher than average industry cyclicality

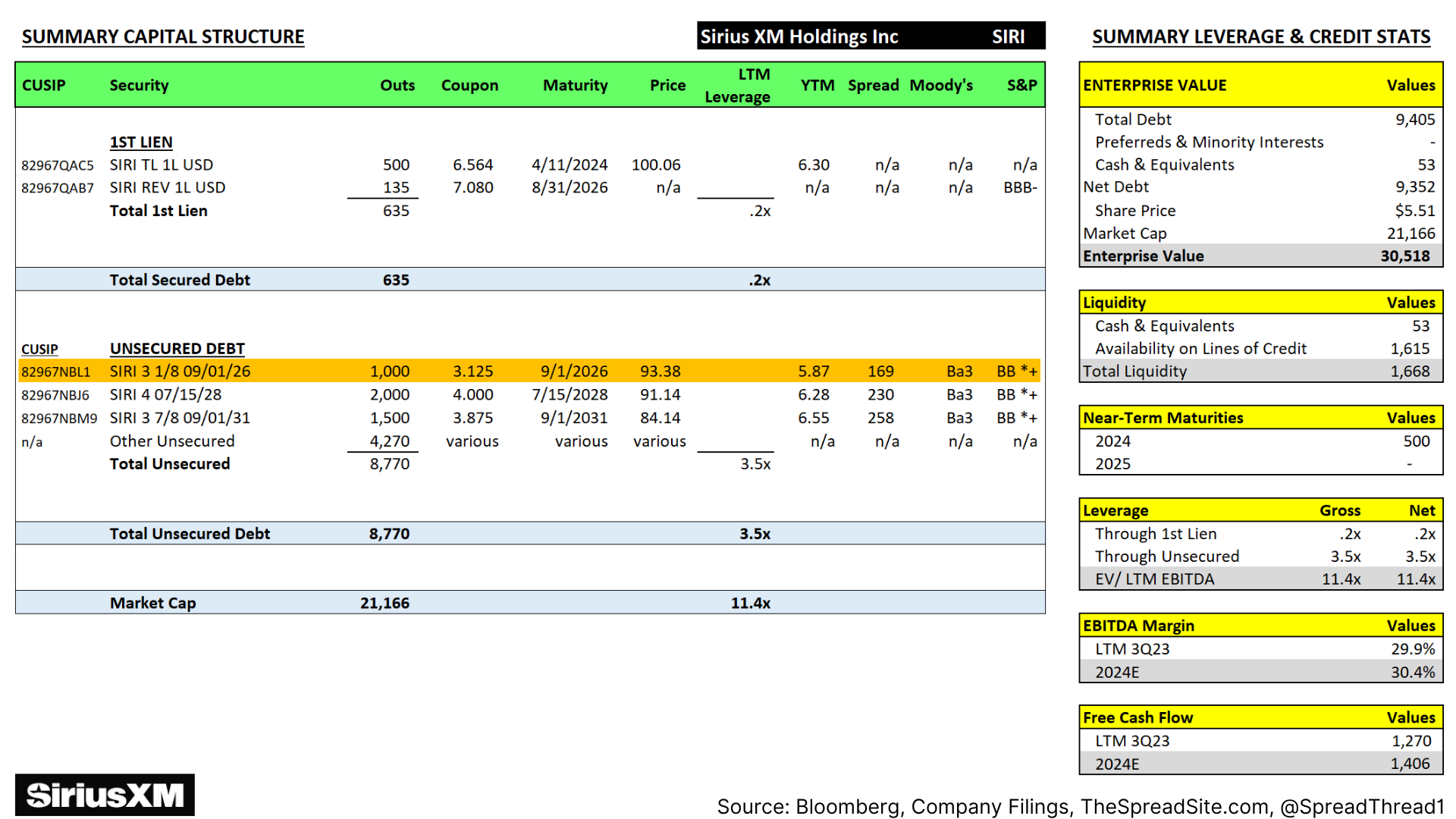

Bond 9: Sirius XM, 3.125% '26

SECTOR: Media

169bp Spread, 5.9% YTM

- Positive: Large valuation gap between unsecureds (3.5x net) and EV/EBITDA of 11.4x

- Positive: High EBITDA margins and FCF conversion

- Risk: Lower overall liquidity relative to short-term maturities through 2026

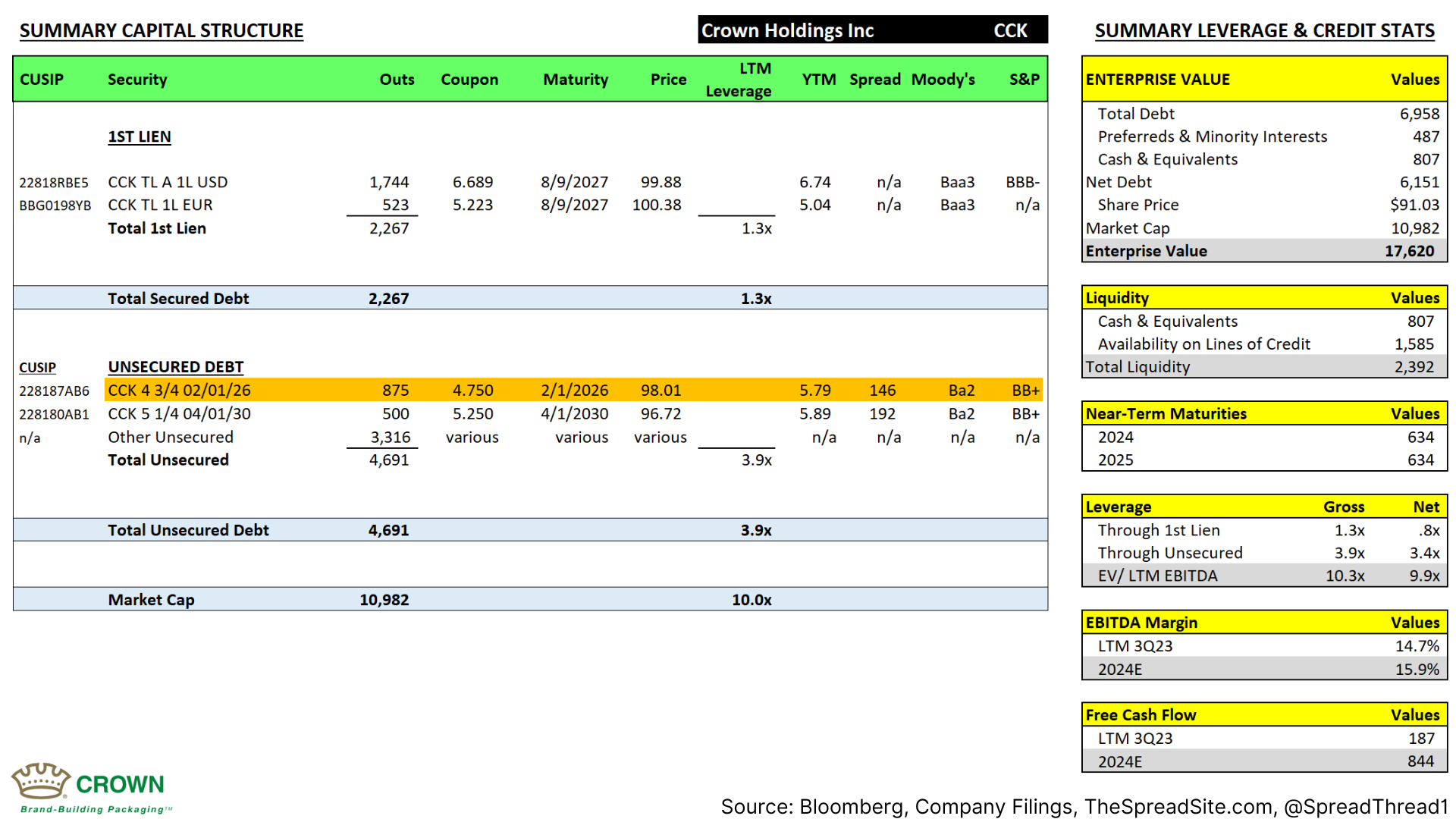

Bond 10: Crown Holdings, 4.75% '26

SECTOR: Packaging

146bp Spread, 5.8% YTM

- Positive: FCF and debt paydown increases significantly in ’24 after a recent expansion is completed

- Positive: Large valuation gap between unsecureds (3.4x net) and EV/EBITDA of 9.9x

- Risk: $2.6b of debt maturities in 2026 (including the chosen bond)

Appendix

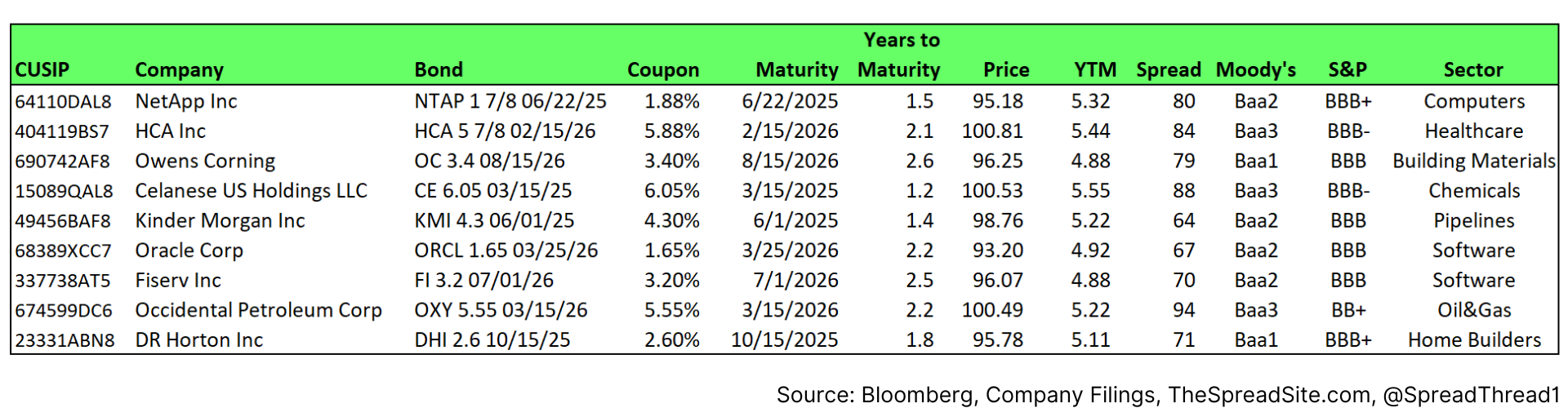

Lastly, here some additional high quality front-end credits that didn’t make the list given spreads that we felt were too tight to include.

Disclosures

Please click here to see our standard legal disclosures.

The Spread Site Research

Receive our latest publications directly to your inbox. Its Free!.

{kind=link}